In a Nutshell

Imagine you lend someone money and they hand you a cheque. You walk to the bank, feeling relieved, and the bank hands it right back. "Insufficient funds." That moment, frustrating as it is, is not the end of the road. In Nepal, bouncing a cheque is a serious legal matter. The person who gave you that cheque can face fines, a criminal record, and even jail time. And you have the law firmly on your side as long as you act in time.

This guide explains everything in plain language: what a cheque bounce actually is, what the law says, what you can do about it, and what happens if you ignore it.

So, What Exactly Is a Cheque Bounce?

When you deposit or present a cheque at the bank, and the bank refuses to give you the quoted amount , that is called a dishonoured cheque. The most common reason and the one the law takes most seriously is that the person who wrote the cheque simply did not have enough money in their account.

Other reasons a bank might reject a cheque include:

● The signature on the cheque does not match the bank's records.

● The cheque has been altered or overwritten.

● The cheque is outdated (usually more than 6 months old) or post-dated.

● The amount written in words and numbers does not match.

● The account has been frozen or closed.

All of these count as dishonour. But a cheque bounce, in the strict legal sense, usually means one specific thing: the money simply was not there.

Why Should You Take This Seriously?

A lot of people in Nepal treat a bounced cheque as an awkward situation to sort out quietly. That is a mistake. Under Nepali law, knowingly writing a cheque when you do not have the funds to cover it is a criminal offence, not just a civil dispute. The person who gave you that cheque can go to jail.

On the flip side, if you are the one who wrote the cheque by mistake, say, you forgot your balance was low, you should also understand the consequences and act fast to make things right before they escalate.

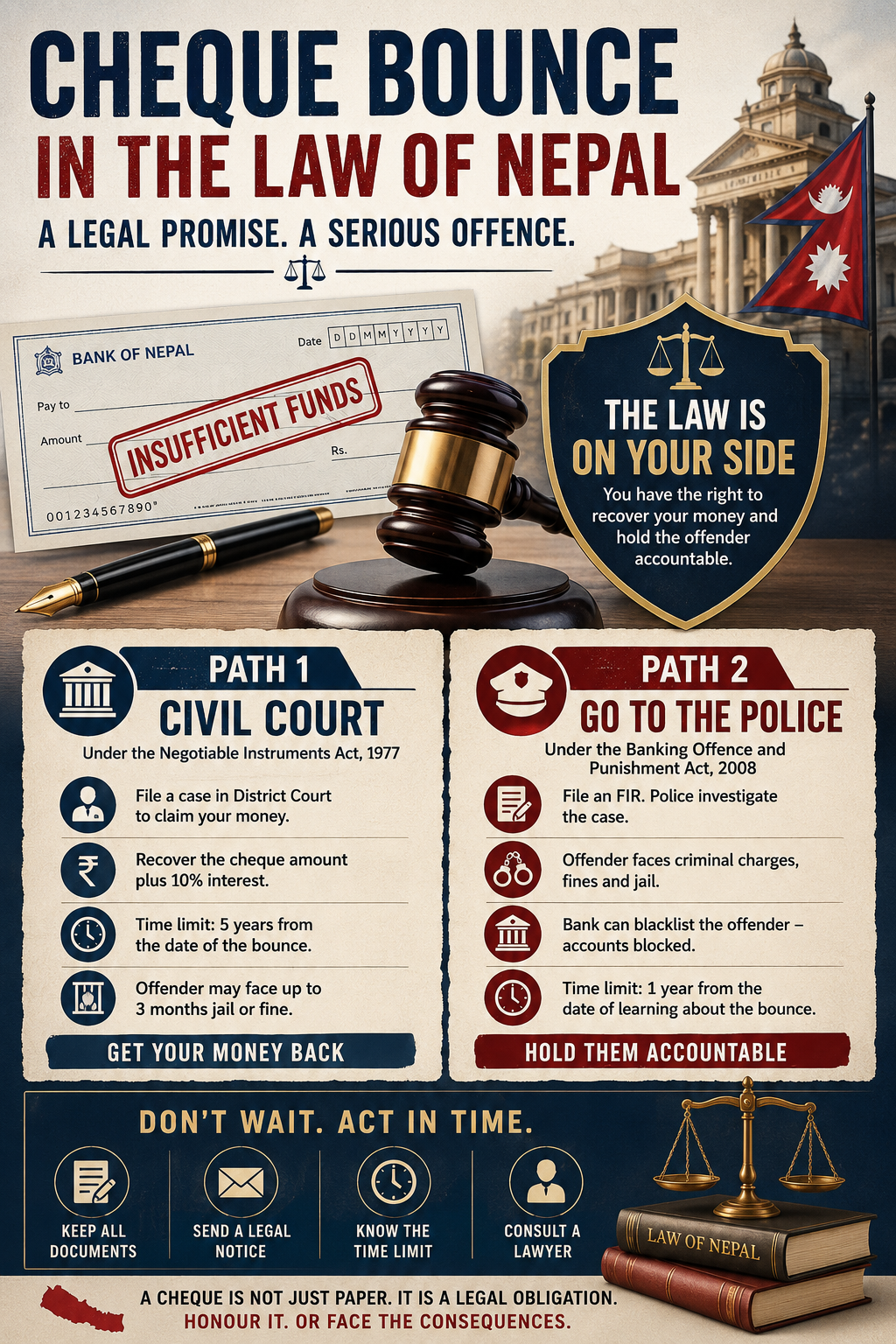

The Two Laws That Protect You

Nepal has two separate laws that deal with cheque bounce. Think of them as two different doors you can knock on:

Door 1 — The Negotiable Instruments Act (1977)

This is the older law. It treats the matter as a money dispute between two people. You go to court, you prove your case, and if you win, the court orders the other person to pay you back with interest. The government is not directly involved. Think of it as suing someone in civil court.

Best for: Getting your money back, especially if you also want 10% interest on top of the cheque amount.

Time limit: You have 5 years from the date of the bounce to file your case.

Door 2 — The Banking Offence and Punishment Act (2008)

This is the stronger, newer law. It treats cheque bounce as a crime against the state, like theft or fraud. You go to the police, they investigate, and the government's attorney prosecutes the case. You do not fight alone; the state fights alongside you.

Best for: Making the other person face criminal consequences, fines, a criminal record, and potentially prison.

Time limit: You must file your police complaint within 1 year of learning about the bounce. Do not wait.

You can actually use both laws at the same time. Many people do it to get their money back, and one to hold the person criminally accountable.

Path 1: Taking Them to Civil Court

Here is how the process works under the older law, step by step in plain terms:

Step 1: File your complaint at the District Court. You write a formal complaint (called a Statement of Claim) explaining what happened and what you want. You submit this to the District Court in the area where the incident took place.

Step 2: The other side gets to respond. The court informs the person who gave you the cheque. They have a chance to explain themselves, maybe they dispute the amount, or claim there was an agreement to wait.

Step 3: Both sides show their evidence. You bring your documents, the bounced cheque, the bank's rejection letter, any messages or receipts. The other side brings theirs. Witnesses can also speak.

Step 4: The judge decides. After hearing everyone out, the judge gives a verdict. If you win, the court orders the other person to pay.

Step 5: If you are unhappy, you can appeal. Not satisfied with the outcome? You can take the case to the High Court.

Step 6: Collecting your money. If the other side refuses to pay even after losing, the court can step in to enforce the payment.

What you can win: Your original cheque amount, plus 10% interest. The other person may also face up to 3 months in jail or a fine of up to NPR 3,000.

Path 2: Going to the Police

This is the route you take when you want the full weight of the law behind you. Here is how it unfolds:

Step 1: Present the cheque to the bank three times. Before filing a police complaint, try depositing the cheque at least three times. Each time, get the bank's written rejection slip. These papers are your evidence.

Step 2: Go to the police and file an FIR. An FIR is simply a formal written complaint to the police. You bring the bounced cheque and the rejection slips. The police write it all down and begin the process.

Step 3: Police investigate. The police look into the matter, they check bank records, contact witnesses, and build a file. This report then goes to the Government Attorney's office.

Step 4: The government files the case in court. The Government Attorney reviews the police report and formally files the case in the District Court on behalf of the state. You no longer carry the burden of prosecution alone.

Step 5: Bail hearing. The person who gave you the bad cheque appears in court. The judge decides whether to grant them bail or keep them in custody while the case runs.

Step 6: Evidence and witnesses. The court goes through the evidence carefully, hears from any witnesses, and examines documents.

Step 7: The verdict. The judge delivers the final decision and determines the punishment.

Step 8: Appeal if needed. Either party can appeal to the High Court, and even the Supreme Court if the matter is serious enough.

Step 9: Enforcement. Once everything is final, the court ensures the verdict is carried out.

Extra tool: You can also ask the bank to blacklist the person who gave you the bad cheque. If the bank agrees, that person's existing accounts get blocked, and they cannot open new ones anywhere in Nepal. This is a powerful pressure tool.

What Punishment Does the Cheque Bouncer Face?

Under the criminal law, the punishment depends on how big the cheque was:

| Cheque Amount | Possible Jail Time |

| Small amounts (general cases) | Up to 3 months + fine equal to cheque value |

| Up to NPR 10 lakh (1 million) | Up to 1 year |

| NPR 10 lakh to 50 lakh | 1 to 2 years |

| NPR 50 lakh to 1 crore | 2 to 3 years |

| Above NPR 1 crore | 3 to 5 years |

On top of jail time, they must repay the full cheque amount. Under the civil law, they also owe you 10% interest.

Which Path Is Right for You?

Here is a simple way to think about it:

Go civil (Negotiable Instruments Act) if:

● Your main goal is to get your money back

● You also want interest on top of what you are owed

● You need more time, you have up to 5 years

Go criminal (Banking Offence and Punishment Act) if:

● You want the person held accountable, not just asked to pay

● You want the police and the government involved

● You want to get them blacklisted from banking

Go to both if:

● The amount is large, and you want every tool available to you

Before You File Anything - A Few Smart Steps

Keep every piece of paper. The original cheque, every bank rejection slip, and any messages where the person promised to pay. This is your case.

Send them a written warning first. Have a lawyer send a formal letter demanding payment within a set number of days. This often resolves the matter without ever stepping into a courtroom — and if it does go to court, it shows you gave them a fair chance.

Do not sit on it. Especially if you are going the criminal route, the 1-year deadline moves fast.

Talk to a lawyer early. Even a single consultation can tell you which path makes the most sense for your situation and how strong your case is.

Common Questions People Ask

1. "What if I accidentally bounced a cheque, I just forgot my balance was low?"

Accidentally bouncing a cheque is different from deliberately doing so. The criminal law specifically requires that you knowingly issue the cheque without funds. However, you

should still contact the other party immediately, repay the amount, and avoid letting it escalate. Intent matters, but courts look at the full picture.

2. "Can we just settle this quietly without going to court?"

Yes, and many cases do get resolved this way. If the person agrees to pay the full amount (and interest, if you negotiated it), you can settle privately at any stage. Just make sure to get the settlement in writing.

3. "What is a bank return memo, and do I really need it?"

Yes, this is the paper the bank gives you when it rejects the cheque. It is your single most important document. Without it, you have no official proof that the cheque bounced. Always ask the bank for this in writing, every single time.

4. "What if they have left the city or are avoiding me?"

Under the criminal route, the court can issue an arrest warrant if the accused cannot be located or is deliberately hiding.

5. "Can I file a case against a company, not just a person?"

Yes. If a business issued the bounced cheque, the individuals responsible for signing it can be held liable personally.

Closing Perspective

A cheque is more than just a piece of paper; it is a legal promise. When someone hands you a cheque, they are telling you: "This money is there, and it is yours." Breaking that promise has real consequences in Nepal.

If you are on the receiving end of a bounced cheque, you are not powerless. The law gives you real options, the ability to recover your money, hold the person criminally accountable, and in serious cases, cut off their access to banking entirely.

The most important thing is not to wait. Time limits are real, evidence fades, and every day you delay gives the other side more room to manoeuvre. Gather your documents, talk to a lawyer, and take that first step.